May 2026 Monthly Market Update

June 8, 2026

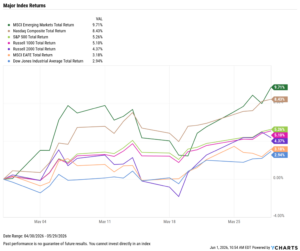

Market Summary: Technology the Standout Winner as All Indices are Positive, Employment Picture Unchanged

Markets rose across the board in May, with the S&P 500 rising 5.3% following its best month since November 2020 in April. Emerging Markets led the way, up 9.7% as all major indices posted returns of more than 2.9%.

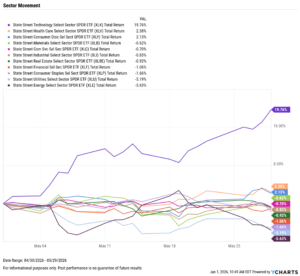

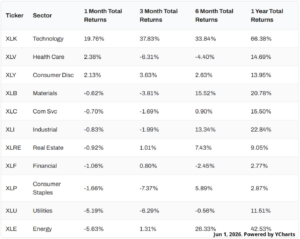

Sector performance was much more divided, with a majority of sectors negative for the month. Technology led by a wide margin, up 20% for the second straight month, more than 16% better than Health Care in second place. Energy lagged for the second consecutive month, down 5.6% as work towards a resolution with Iran hangs in the balance.

The Federal Reserve’s next meeting is scheduled for June 17th, though the market is pricing in more than a 99% chance that rates remain unchanged. Nonfarm payrolls grew by 115,000 jobs, and the unemployment rate remained unchanged at 4.3%.

The Median Sales Price of Existing Homes increased to $417,700, while the US inflation rate rose 0.50% MoM to 3.8%. Core inflation experienced a more modest increase of 0.20% to 2.80%.

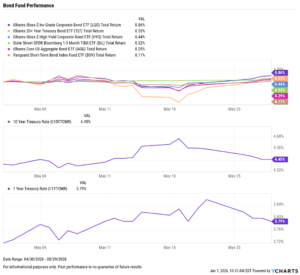

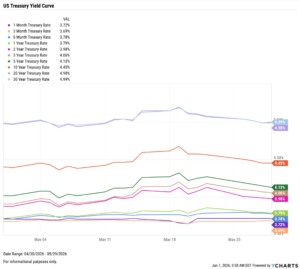

Treasury yields rose slightly across the curve in May. The 3-month, 20- and 30-year all increased by just 1 basis point for the month, while the 6-month increased by seven basis points.

Chappell Wealth Watch! A New Era at the Fed

On May 15th, 2026, Jerome Powell’s tenure as Fed Chair ended after eight years, as Kevin Warsh was sworn in as the 17th Chair in the Federal Reserve’s 113-year history.

Warsh takes over with the Federal Funds Rate at 3.75%, and markets are forecasting a more than 50% chance that this remains unchanged through the end of 2026. These projections reflect uncertainty around Warsh’s policy direction, compounded by the highest level of internal FOMC dissent since 1992 and rising inflation. He will inherit a divided committee navigating an increasingly unsettled economic backdrop.

While inflation and geopolitical risks are real, and some degree of volatility surrounding this transition is to be expected, across the five leaders who each inherited different economies and challenges since 1979, the S&P 500 has returned more than 3,840% total.

The noise surrounding a Fed transition is not a signal to abandon the plan, and in moments like this, an advisor’s most important role is helping clients stay disciplined long enough for any uncertainty to work in their favor.

Download YCharts’ latest deck, A New Era at the Fed, to give clients the historical context they need, address the questions they’re facing, and keep them focused on the long-term plan.

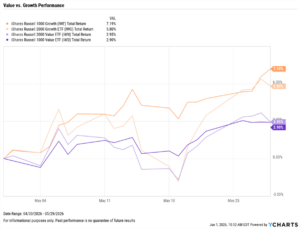

Equity Performance: All Major Indices Positive, Technology Surges another 20% as Growth Styles Lead

Value vs. Growth Performance

US Sector Movement

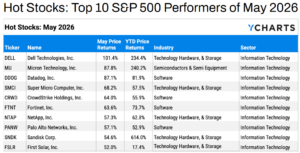

Top 10 S&P 500 Performers of May 2026

10 Worst S&P 500 Performers of May 2026

Economic Data Overview: Unemployment Holds, Inflation Worries as Oil Remains the Key

Employment

The unemployment rate held steady at 4.3% for the second consecutive month, and the U.S. economy added 115,000 jobs according to the most recent nonfarm payrolls report, well above the Dow Jones estimate of 55,000. The US Labor Force Participation Rate decreased by 0.1 percentage points for the third straight month to 61.80%.

Consumers and Inflation

The US inflation rate increased by 0.50% MoM to 3.8%, the highest reading since May 2023. Core inflation increased by 0.20% MoM to 2.80%. The CME FedWatch tool indicates more than a 99% chance that the FOMC will hold rates at its next meeting on June 17th, with market pricing increasingly reflecting the possibility of a hike later in 2026. Rates remain at 3.50–3.75%, as the Fed enters Kevin Warsh’s tenure as Fed Chair, following his Senate confirmation on May 14th.

Production and Sales

The US ISM Manufacturing PMI went unchanged, sitting at 52.7 for the second consecutive month. The Services PMI fell by 0.4 points, though still sitting well above the expansion threshold. The YoY US Producer Price Index rose for a fourth month straight to 6.0%, its highest reading since December 2022, while US Retail and Food Services Sales continued to increase MoM, though at a slower pace of 0.49%.

Housing

Existing Home Sales were nearly flat MoM, ticking up just 0.25%, snapping a streak of four consecutive months with moves of 2.5% or greater in either direction. The Median Sales Price of Existing Homes increased by $8,600 to $417,700, continuing to hold above $400,000 for a second straight month.

Mortgage rates rose in May, ending the month at 5.87% for the 15-year and 6.53% for the 30-year. US New Single-Family Home Sales declined MoM, falling 6.18%, though well off the pace of January’s historic 20% drop.

Commodities

Gold slipped further in May, with SPDR Gold Shares (GLD) falling 1.54% to end the month at $410.80 per share. Silver reversed course, gaining 2.51% on the month.

Oil prices remained top of mind in May, though a fragile ceasefire framework between the US and Iran helped ease some pressure. Brent crude finished the month at $102.75 and WTI at $97.63 per barrel, both down sharply from April’s highs. Consumers continue to feel the pain at the pump, with the US Retail Gas Price rising further above $4.50 per gallon throughout May.

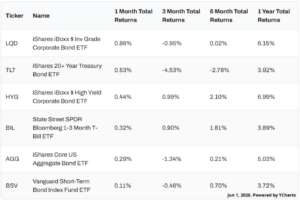

Fixed Income Performance: Insights into Bond ETFs & Treasury Yields

US Treasury Yield Curve

Bond Fund Performance